The US healthcare system is complex, with a mix of private and public funding. Below is a breakdown of its key components so you could understand it better.

Who Pays for Healthcare?

Most people in the US do not receive free healthcare. Payment comes from three main sources:

- Insurance: Many people get health insurance through their jobs. Others purchase it privately.

- Government Programs: The government provides Medicare for seniors and Medicaid for low-income families.

- Out-of-Pocket: Those without insurance must pay medical bills directly, which can be very expensive.

Health Insurance Basics

Health insurance works as a contract where you pay a monthly premium, and the insurance company helps cover medical costs. However, you may still need to pay:

- Deductibles: What you pay before insurance kicks in.

- Copays: Fixed fees for visits or medications.

- Coinsurance: A percentage of costs after meeting your deductible.

Some plans are more comprehensive but come with higher premiums.

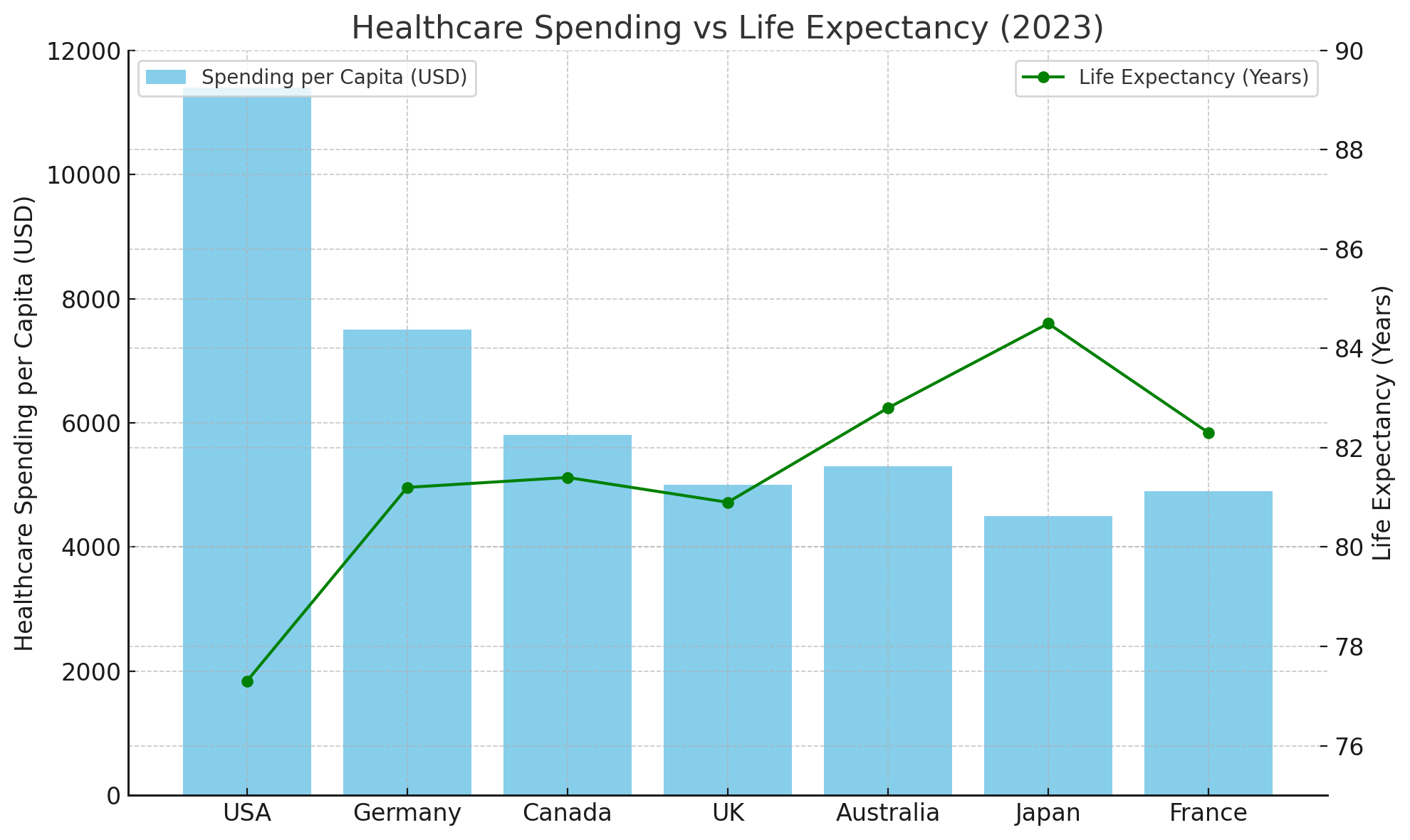

U.S. Healthcare Spending Infographic. The U.S. shows the highest spending but relatively low life expectancy, highlighting inefficiencies in the system.

Types of Insurance Plans

There are several ways to get health insurance:

1. Employer-Sponsored Insurance: Provided by your workplace, often with shared costs.

2. Private Insurance: Purchased individually through marketplaces like Healthcare.gov.

3. Government Programs:

- Medicare: For those over 65 or with certain disabilities.

- Medicaid: For low-income individuals and families.

- VA Healthcare: For veterans.

What Happens If You Don’t Have Insurance?

Without insurance, you’re responsible for all medical bills. Emergency care is required by law, but it’s costly. Some hospitals offer charity care programs, but unpaid bills can lead to significant debt.

Common Problems in the US Healthcare System

The system faces several challenges:

- High Costs: Medical care in the US is more expensive than in most other countries.

- Confusion: Insurance plans vary widely, making it hard to predict costs.

- Access Issues: Not everyone can afford insurance or care.

How to Save on Healthcare

Here are practical ways to reduce costs:

Use government-funded insurance plans available in your state, like Community Health Plan in Washington.

Use government-funded insurance plans available in your state, like Community Health Plan in Washington.- Use in-network doctors and facilities to get lower rates.

- Compare prices for medications and procedures.

- Utilize free or low-cost clinics if eligible.

- Focus on preventative care, such as vaccines and screenings.

What is the Affordable Care Act (ACA)?

The ACA, also known as Obamacare, was introduced to expand healthcare access. It:

- Created marketplaces for buying insurance, such as Healthcare.gov and state-specific exchanges like Covered California.

- Provided subsidies to make insurance more affordable for low-income individuals.

- Ensured coverage for pre-existing conditions.

Key Terms to Know

To navigate the system, understanding these terms is crucial:

- Premium: Your monthly insurance payment.

- Deductible: The amount you pay before insurance starts covering costs.

- Copay: A set fee for services or medications.

- Out-of-Pocket Maximum: The most you’ll pay in a year before insurance covers 100% of costs.

Emergency Care in the US

Hospitals must provide emergency care, even if you can’t pay. This is required by the Emergency Medical Treatment and Labor Act (EMTALA). However, not being able to pay doesn’t mean the cost disappears:

- Hospitals will treat you first and figure out how to bill you later. They may ask for a name, address, or anything you’re willing to provide. If you give false info, they’ll bill whoever they can track down at that address.

- No ID? They’ll still try to pursue collections based on whatever details they have, even incomplete ones.

- If they absolutely can’t identify or bill you, the costs often get shifted to charity programs, government reimbursements, or higher charges for insured patients.

- Ambulances work differently. Without ID or insurance, expect an astronomical bill directly mailed to whatever info you gave – or no service at all if they aren’t bound by emergency laws.

- If ambulances are bound by emergency laws in your state, they must transport you and stabilize your condition regardless of your ability to pay or provide ID.

Bottom line: No ID makes billing you trickier, but the system always finds ways to pass the cost somewhere else.

Healthcare for Kids

Children in the US can access free or low-cost healthcare through programs like Medicaid and CHIP, which are available based on family income. Lawfully residing immigrant children may qualify for these programs in most states.

For undocumented children, options include Emergency Medicaid, state-specific programs (e.g., in California or New York), community health centers, and school-based clinics. Learn more at Medicaid, CHIP, or HRSA Health Centers.

Why Is U.S. Healthcare So Expensive?

The U.S. spends more on healthcare than any other country due to several factors:

- Administrative Costs: Around 25% of healthcare spending goes to administrative expenses like billing, much higher than in other countries.

- High Medical Prices: Doctors, hospitals, and procedures cost significantly more than in other nations.

- Expensive Prescription Drugs: Americans pay nearly double for medications compared to other countries due to weak pricing regulations.

- Advanced Technology & Defensive Medicine: Cutting-edge treatments and overuse of tests to avoid lawsuits drive costs even higher.

These factors, coupled with fragmented care and inefficiencies, make U.S. healthcare uniquely expensive and challenging to reform.

Key Takeaways

- Have a medical insurance in the US.

- Understand your insurance plan and know what it covers.

- Always ask about costs before treatments.

- Healthy lifestyle and preventive measures help to avoid problems.

Leave A Comment